At last week’s FOMC assembly, Jerome Powell said, “We believe economic problems are weighing on the economy.”

His comments feel practical, given the adhering to:

- The Fed is lowering its stability sheet (QT).

- The Fed Funds amount is at its maximum stage in around 15 yrs.

- Home loan premiums are about 7%, 3-4% previously mentioned pre-pandemic ranges.

- Credit rating card interest rates are 20% or much more.

- Car loans assortment in between 7% and 10%

- Purchaser mortgage development, excluding the pandemic, is down to levels past viewed over ten many years ago.

- Remarkable Commercial & Industrial (C&I) financial loans are declining.

Powell’s statement indicates that fiscal disorders are tight. On the other hand, they are uncomplicated dependent on the Fed’s definition of economic disorders. If Powell doesn’t value the variance between money and borrowing problems, we must believe most investors do not both.

As we will make clear, there is a large big difference involving fiscal and borrowing circumstances. Equally truly worth considering is that the latest mixture of effortless financial problems and restricted borrowing disorders can make monetary policy challenging for the Fed to harmony.

Contents

What Are Money Conditions?

The St. Louis Federal Reserve defines money ailments as follows:

“Actions of fairness prices (also normally referred to as inventory selling prices), the strength of the U.S. dollar, market volatility, credit rating spreads, lengthy-time period interest costs, and other variables.”

Economical circumstances are inclined to be uncomplicated when investors are optimistic and speculative. Let’s glance at the four crucial measures in the St. Louis Fed definition to recognize why financial circumstances are simple now.

Fairness Prices: The S&P 500 is up 38% since 2023 and 10% by means of the initial 3 months of 2024.

U.S. Greenback: The greenback index has been rather flat because 2023 and the calendar year to date.

Market place Volatility: The VIX volatility index has been hovering amongst 12 and 15 this 12 months. That is about one particular common deviation down below the ordinary VIX looking through of 19.32 around the previous 35 several years.

Credit Spreads: The BBB investment decision quality produce is only 1% previously mentioned a equivalent maturity Treasury. This sort of is the tightest distribute considering that the 1990s.

Extended-Phrase Desire Prices: Lengthy-phrase interest costs have been appreciably increased than common more than the earlier few a long time and at amounts final viewed ahead of the economic crisis in 2008. Having said that, they are about 1% reduce than their peak last calendar year.

Fairness price ranges, marketplace volatility, and credit spreads point to incredibly uncomplicated economic problems, and we might also characterize their degrees as speculative.

The greenback has experienced little impact on economic situations as it has been reasonably stable.

Very long-expression fascination premiums place to tighter monetary conditions, albeit easing more than the past six months.

The base line is that monetary disorders are quick in big aspect mainly because sturdy sentiment in the equity and credit history marketplaces a lot more than offsets larger fascination premiums.

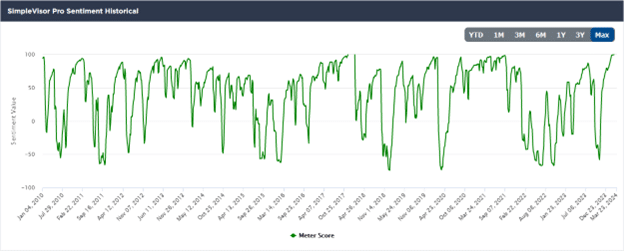

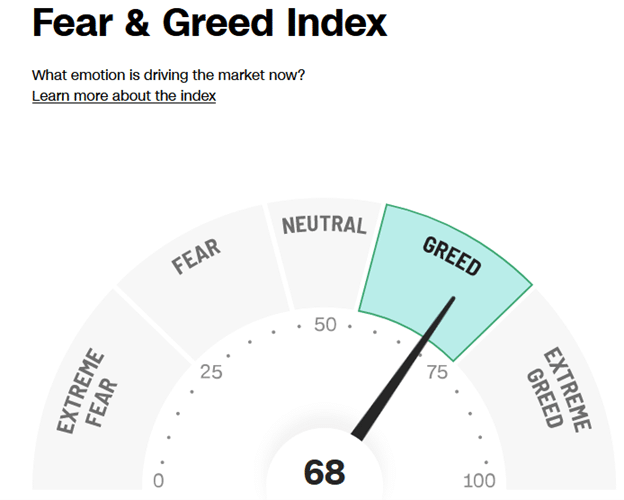

As shown down below, our proprietary SimpleVisor Sentiment indicator is at its greatest stage, and the CNN Panic & Greed Index is closing in on severe greed.

What Are Borrowing Problems?

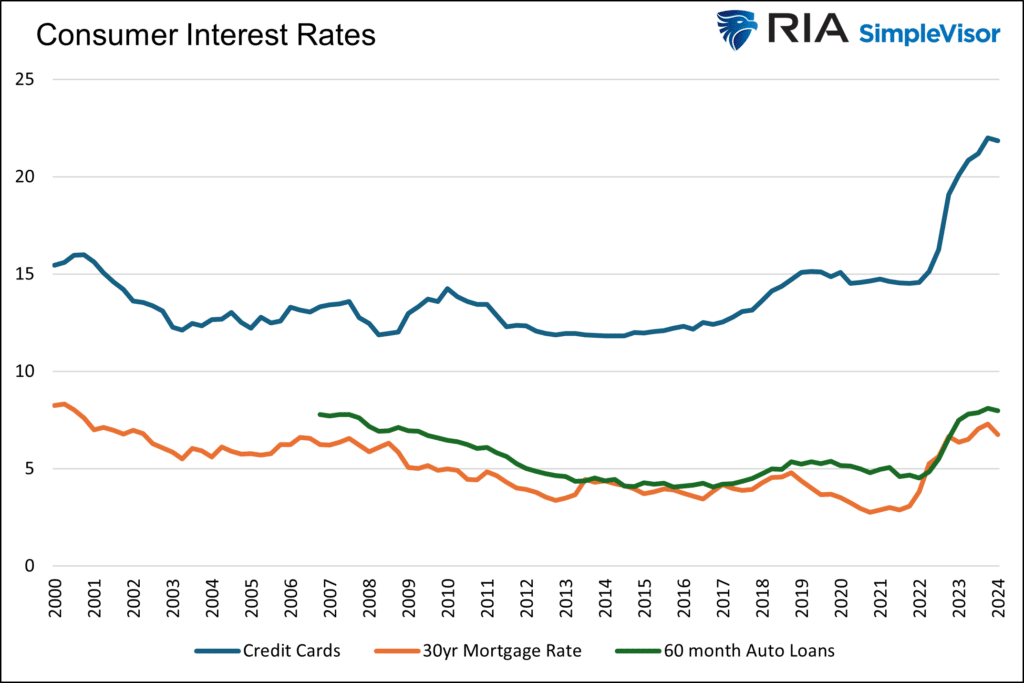

In contrast to monetary conditions, borrowing ailments are significantly from simple. The two graphs below emphasize the financial pressure on consumer and corporate borrowers.

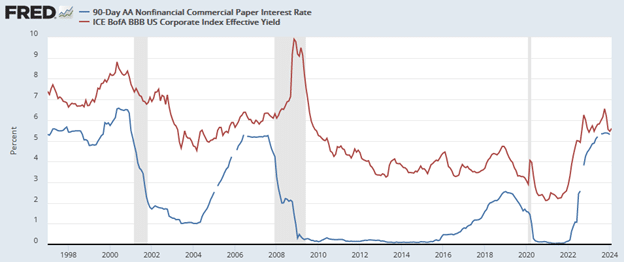

Credit score card curiosity charges are more than 20% and about 5% higher than the optimum in the past 24 decades. House loan and car mortgage interest rates are up to stages not noticed in at the very least fifteen years.

The subsequent graph shows that 90-day business paper financial loans and yields on BBB-rated company bonds are at their highest ranges since the money crisis.

What Can And Can’t The Fed Take care of?

The Fed plays a crucial part in directing money and borrowing conditions. At times, like currently, money and borrowing situations can be at odds with each individual other, which helps make the Fed’s task of taking care of monetary coverage more complicated.

The marketplace’s perception of the Fed’s stance, hawkish or dovish, and a lot more importantly, forecasts of how they may possibly improve coverage can heavily influence industry sentiment and financial circumstances.

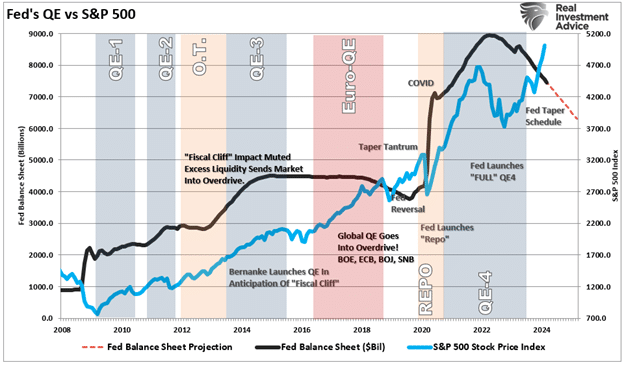

For instance, a powerful correlation exists in between QE and better inventory returns, lower volatility, and tighter credit spreads. The partnership takes place in aspect due to the psychology of investors. Nonetheless, it’s also a function of the liquidity the Fed results in when conducting QE. For comparable good reasons, decreased charges are believed to be helpful for marketplaces.

The Fed has a heavier hand in determining borrowing ailments. By taking care of its Fed Money rate, the Fed sets the tone for extensive-phrase interest charges and significantly influences shorter-time period costs. More, QE and QT can include or subtract liquidity from the markets, instantly impacting the provide and demand from customers of liquidity accessible to all markets.

Powell’s Predicament

Economic situations have eased significantly as investors priced out the odds of amount raises and have started off pricing in price cuts. The mixture of decrease curiosity rates and quite possibly significantly less QT, coupled with sturdy economic progress, is the goldilocks situation driving investors’ sentiment larger. This happens irrespective of exceptionally restricted borrowing conditions and a hawkish monetary policy.

Currently, the Fed does not want economic problems to relieve further as the prosperity result of solid markets can have an inflationary impulse. They could hike prices or even discuss of expanding fees to weigh on economic conditions. On the other hand, with tight borrowing circumstances and the possible that the lag impact of prior rate hikes will finally induce a recession, they show up to be in no person’s land.

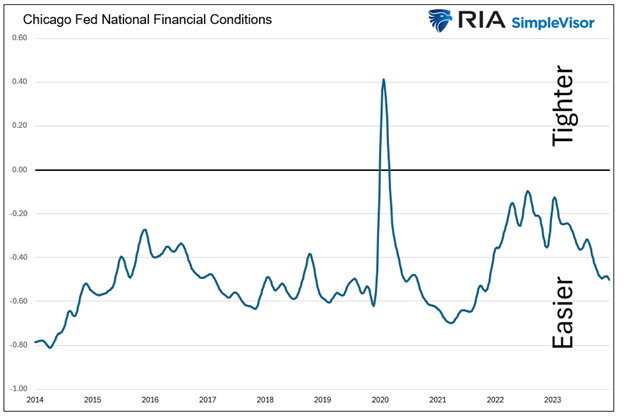

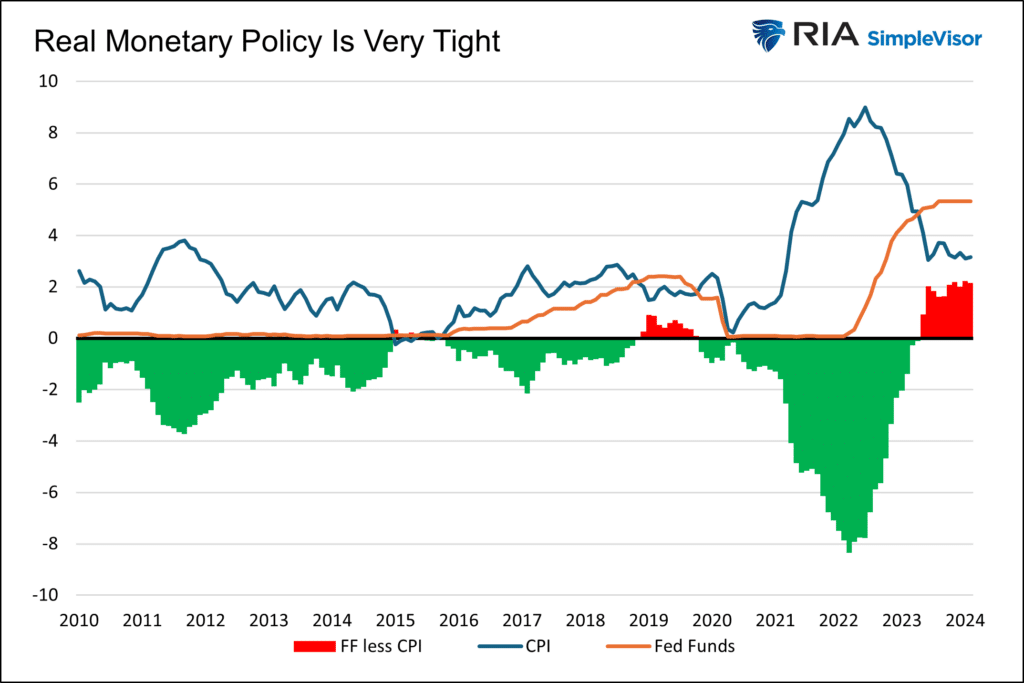

As we share under, on a true basis, the Fed’s coverage stance is the tightest it has been in fifteen a long time.

An additional Fed Predicament Coming Shortly

Sentiment and liquidity generate markets in the brief run. The two have supported larger inventory prices and mania-like buying and selling in AI stocks and cryptocurrencies.

Nonetheless, that could be transforming. As we be aware in Liquidity Challenges, extra liquidity is speedily draining from the financial program. The Fed knows the situation and may perhaps be known as upon to offer with a liquidity shortfall. QT reductions and/or decrease premiums would simplicity liquidity issues. But, accomplishing so, in particular if the financial system stays sturdy and sector sentiment is potent, would risk even more easing of financial disorders, which in turn might keep inflation sticky at latest amounts.

Summary

The Goldilocks economic climate, coupled with the close of the amount mountaineering cycle, has buyers giddy, which eases financial disorders. Ironically, though some of the least complicated economical disorders in the final ten several years have existed, borrowing conditions remain really tight.

The Fed should harmony these two ailments, which is tricky as they can counteract each and every other. Threading the eye of this needle may possibly establish problematic given that inflation stays way too superior and, far more not too long ago, is displaying some symptoms of becoming sticky.

The article Money Problems Butt Heads With Borrowing Situations appeared to start with on RIA.

{kind=link}