In the most recent report from FINRA, margin credit card debt levels have surged as bullish investors leverage their bets in the fairness marketplace. The boost in leverage is not astonishing, as it represents enhanced hazard-taking by investors in the stock marketplace.

We earlier mentioned that valuations, in the shorter term, reflect trader optimism. In other words, as price ranges enhance, buyers rationalize why spending extra for existing earnings is rational.

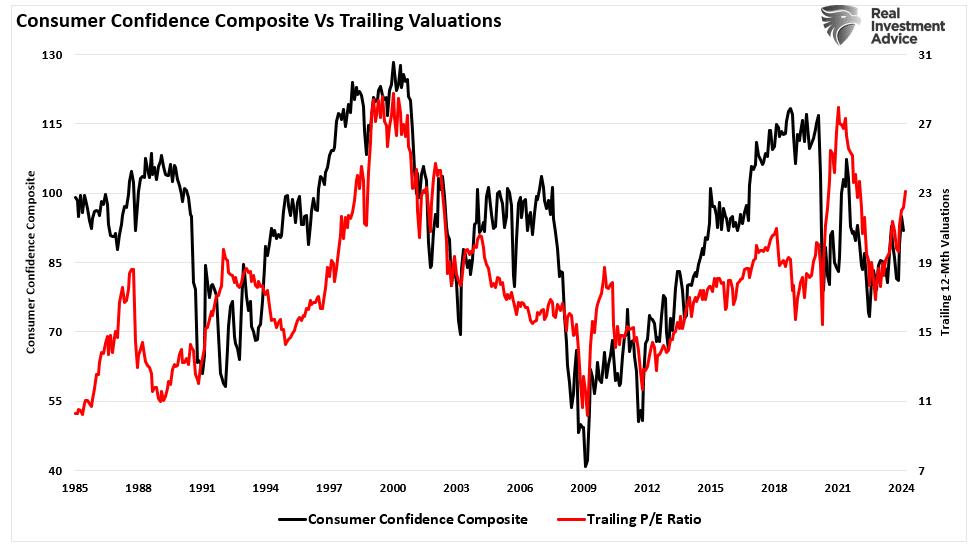

“Valuation metrics are just that – a evaluate of present-day valuation. Far more importantly, when valuation metrics are excessive, it is a far better evaluate of ‘investor psychology’ and the manifestation of the ‘greater fool concept.’ As proven, there is a significant correlation amongst our composite buyer self esteem index and trailing 1-yr S&P 500 valuations.”

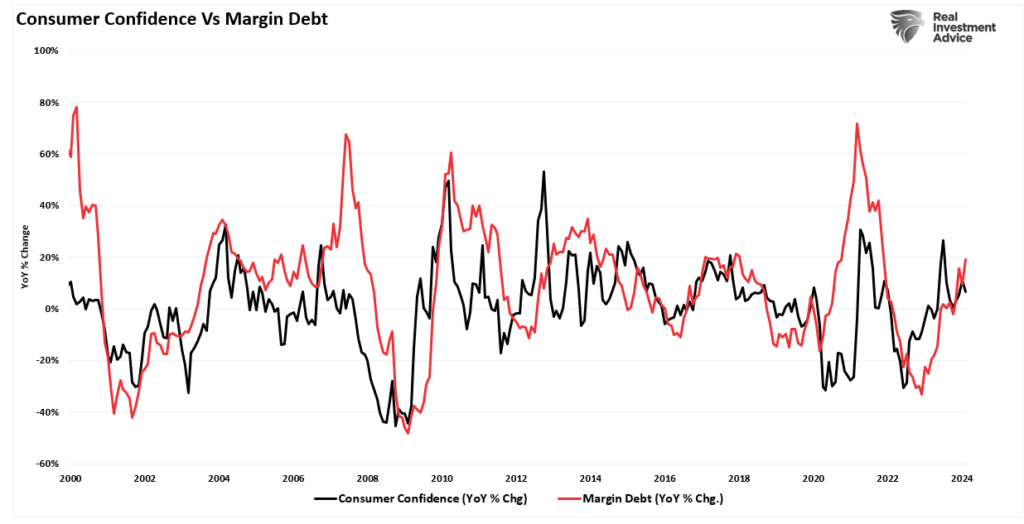

The very same retains for margin personal debt. Unsurprisingly, as client confidence enhances, so does the speculative need for equities. As inventory marketplaces boost, the “dread of lacking out” turns into a lot more common. These types of boosts demand from customers for equities, and as selling prices increase, investors take on a lot more hazard by introducing leverage.

Adding to that exuberance is the enhanced desire for share repurchases, which has been a primary source of “shopping for” given that 2000. As CEO self esteem enhances, a byproduct of elevated consumer self-assurance, they maximize the need for share repurchases. As buybacks enhance asset rates, investors acquire on much more leverage and enhance publicity as a digital spiral develops.

On the other hand, really should buyers be scared of mounting margin credit card debt?

A Byproduct Of Exuberance

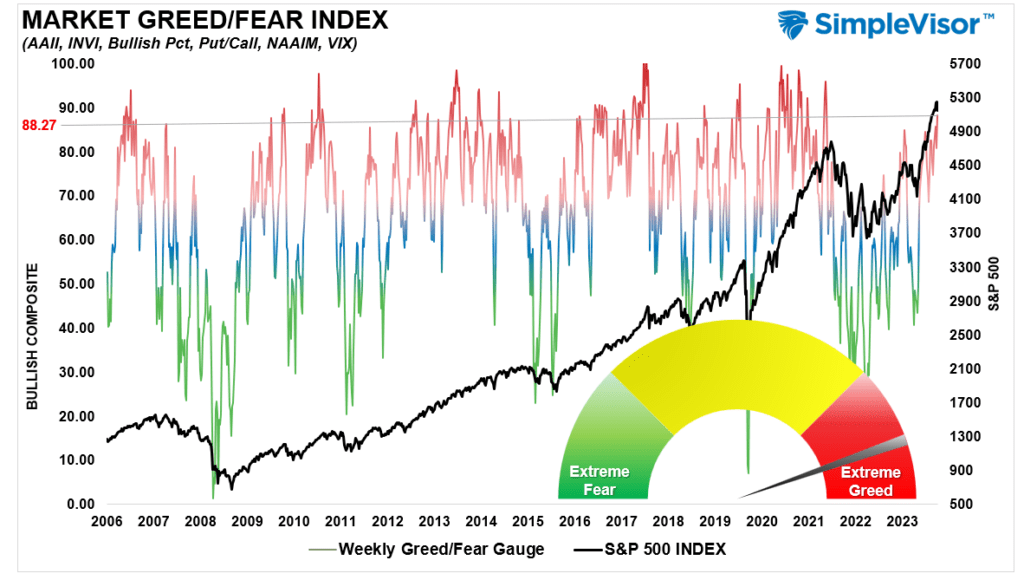

Prior to we dig additional into what margin debt tells us, let’s start off with exactly where we are at the moment. There is clear evidence that traders are when yet again remarkably exuberant. The “Anxiety Greed” index under differs from the CNN measure in that our design actions positioning in the marketplace by how significantly expert and retail investors are exposed to fairness hazard. Currently, that publicity is at ranges linked with investors becoming “all in” the equity “pool.”

As Howard Marks observed in a December 2020 Bloomberg interview:

“Fear of missing out has taken more than from the dread of shedding revenue. If people today are danger-tolerant and worried of remaining out of the current market, they purchase aggressively, in which scenario you just cannot uncover any bargains. That’s the place we are now. Which is what the Fed engineered by placing prices at zero…we are again to wherever we had been a calendar year ago—uncertainty, future returns that are even lower than they had been a year ago, and higher asset selling prices than a calendar year in the past. People are again to getting to just take on far more threat to get return. At Oaktree, we are back to a cautious technique. This is not the variety of natural environment in which you would be buying with each arms.

The future returns are very low on all the things.”

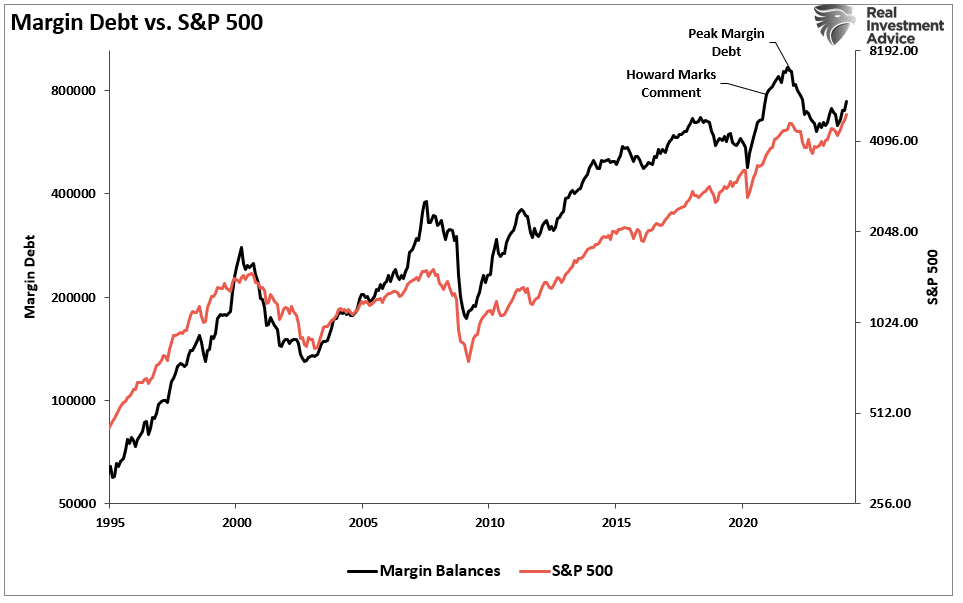

Of study course, in 2021, that market continued its reduced volatility grind larger as investors took on rising margin debt ranges to chase increased equities. Nonetheless, this is the very important position about margin financial debt.

Margin credit card debt is not a technological indicator for investing markets. What it represents is the total of speculation occurring in the market. In other words and phrases, margin financial debt is the “gasoline,” which drives marketplaces higher as the leverage offers for the further obtaining electric power of belongings. On the other hand, leverage also will work in reverse, as it provides the accelerant for much more substantial declines as loan providers “power” the sale of property to go over credit rating lines with no regard to the borrower’s position.

The previous sentence is the most significant. The challenge with margin debt is that the unwinding of leverage is NOT at the trader’s discretion. That course of action is at the discretion of the broker-sellers that prolonged that leverage in the to start with put. (In other words, if you don’t promote to protect, the broker-dealer will do it for you.) When loan companies panic they may well not recoup their credit history traces, they drive the borrower to put in additional hard cash or market property to go over the credit card debt. The challenge is that “margin phone calls” generally come about simultaneously, as slipping asset selling prices influence all lenders concurrently.

Margin credit card debt is NOT an problem – right up until it is.

As proven, Howard was at some point appropriate. In 2022, the decline wiped out all of the prior yr’s gains and then some.

So, wherever are we presently?

Margin Financial debt Confirms The Exuberance

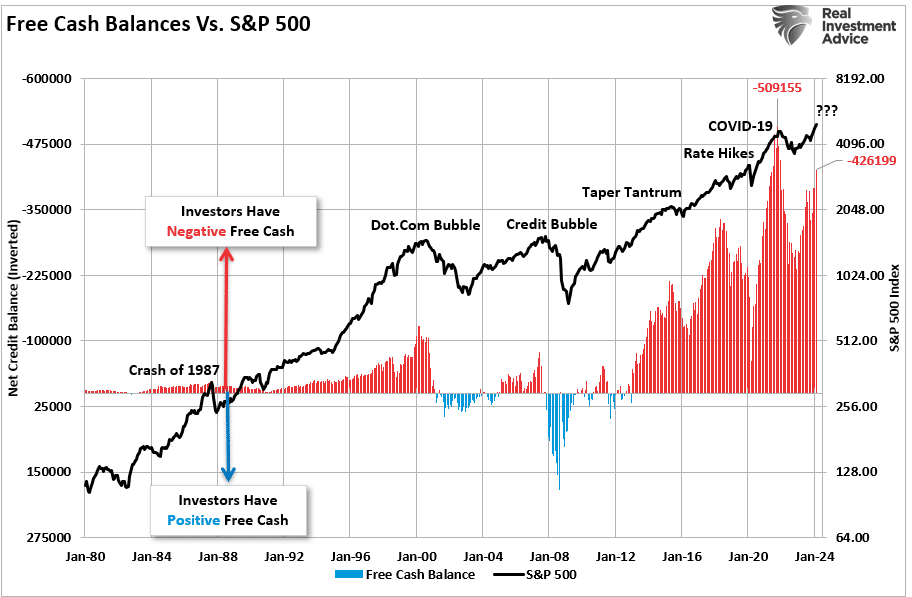

As noted, margin debt supports the progress when marketplaces are climbing and traders are getting on further leverage to enhance getting electricity. Consequently, the modern increase in margin debt is unsurprising as investor exuberance climbs. The chart demonstrates the marriage involving hard cash balances and the market. I have inverted absolutely free hard cash balances, so the romantic relationship between raises in margin financial debt and the market is much better represented. (No cost dollars balances are the big difference involving margin balances fewer dollars and credit rating balances in margin accounts.)

Note that throughout the 1987 correction, the 2015-2016 “Brexit/Taper Tantrum,” the 2018 “Fee Hike Mistake,” and the “COVID Dip,” the market place by no means broke its uptrend, AND money balances hardly ever turned optimistic. The two a crack of the soaring bullish trend and constructive free money balances have been the 2000 and 2008 bear market hallmarks. With destructive money balances shy of another all-time higher, the up coming downturn could be one more “correction.” On the other hand, if, or when, the extensive-expression bullish craze is damaged, the unwinding of margin debt will incorporate “fuel to the fireplace.”

Though the instant reaction to this examination will be, “But Lance, margin debt isn’t as higher as it was formerly,” there are many distinctions amongst nowadays and 2021. The lack of stimulus payments, zero curiosity costs, and $120 billion in month to month “Quantitative Easing” are just a couple. Nevertheless, some glaring similarities exist, which include the surge in detrimental income balances and extreme deviations from prolonged-time period usually means.

In the limited term, exuberance is infectious. The additional the market rallies, the a lot more chance traders want to acquire on. The situation with margin personal debt is that when an function at some point takes place, it creates a rush to liquidate holdings. Since margin credit card debt is a perform of the value of the fundamental “collateral,” the pressured sale of belongings will minimize the value of the collateral. The decrease in benefit then triggers even more margin calls, triggering far more providing, forcing far more margin phone calls, and so forth.

Margin personal debt levels, like valuations, are not practical as a marketplace-timing unit. Even so, they are a important indicator of marketplace exuberance.

Whilst it may perhaps “truly feel” like the marketplace “just received’t go down,” it is well worth remembering Warren Buffett’s sage terms.

“The market place is a large amount like intercourse, it feels greatest at the close.”

The write-up Margin Personal debt Surges As Bulls Leverage Bets appeared 1st on RIA.

{kind=link}